Originally published in Unchained.com.

Unchained, the US Collaborative Custody partners of Bitcoin Magazine is also a sponsor for related content. Visit Unchained to learn more about the services they offer, their custody products and how Unchained is related with Bitcoin Magazine. our website.

The term “you don’t see it often” “Roth IRA” In 2021, the $5 billion Roth IRA piggybank of tech investor Peter Thiel was featured in headlines. How did he manage it? Answer: alternative investments. He invested in tech startups at an early stage using a self directed IRA. It’s a loophole, right? Possibly. This happened. And it attracted attention. Further scrutiny of the IRA could be conducted.

“Thiel has taken a retirement account worth less than $2,000 in 1999 and spun it into a $5 billion windfall.” – ProPublica (2021)

Look at the six most common risks of self-directed IRAs and checkbook IRAs. How they might apply to Bitcoin and why more regulation could be coming. We need to first define the terms we use and then differentiate between IRAs.

There are many different IRA structures

IRA can take on different forms. “every square is a rectangle, but not all rectangles are squares” It depends on the way you want to do it. IRAs can be Traditional (pre-tax) or Roth (post-tax) regardless of custodial relationship/structure. All IRAs have a custodial relationship. Custodians are licensed individuals who manage IRAs. financial The institution that oversees and administers the IRA.

Brokerage and bank IRAs

The most common and familiar types of IRAs include brokerage and bank IRAs. Investors can invest in securities such as stocks, bonds and ETFs as well as bank products like CDs and deposit accounts. You can choose from Fidelity or TD Ameritrade IRAs. This includes the IRAs offered by Charles Schwab, Fidelity and TD Ameritrade. Unchained IRA This structure is the closest in hierarchy to that of this.

Self-directed IRA

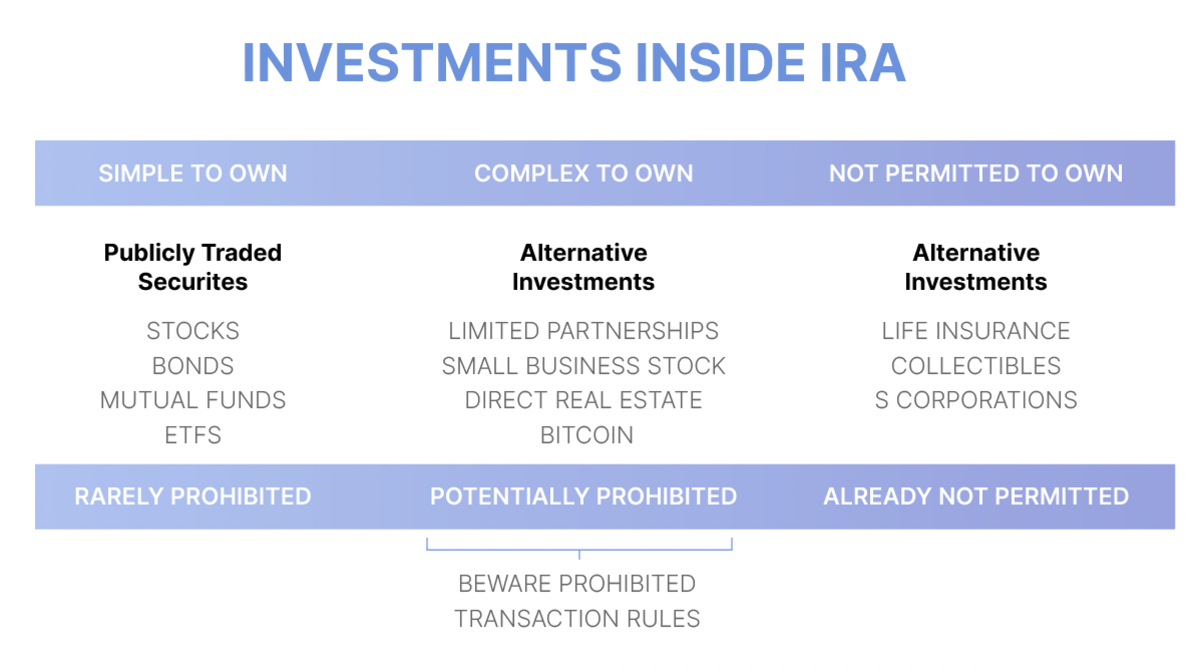

Self-directed IRAs are custodial IRAs where the custodian offers a wider range of investment choices than traditional brokerage assets and banks (stocks bonds CDs etc.). The self-directed IRA allows investors to invest in assets that are not traditional, such as real estate and businesses. It also includes private loans, tax liens or liens on property, precious metals and digital assets. While the IRS hasn’t published a list of all investments allowed, there are a number that it does allow. are not allowed (collectibles, life insurance, certain derivatives, S-Corps, etc.).

Checkbook IRA

A subset of self directed IRAs, checkbook IRAs. The term “checkbook IRA” This is not standard. However, it refers to a self directed IRA which allows an account holder control of their investments by using a check-book account. This account holder then has the option to invest IRA funds by just writing a cheque.”checkbook control”). With additional choices of investments comes increased responsibility in terms of administration. There is also legal ambiguity regarding whether this structure can still be considered a tax-exempt IRA.

IRA Non-checkbook Self-directed

The custodian is the only person who can approve a transaction before it’s made. The custodian must review and accept the title of the asset before the investor can make any investment. They were used to invest in real estate, private equity and other investments. However, they began gaining in popularity after additional legal uncertainty arose in regards to checkbook IRAs late in 2021.

Watch out for these risks when using an IRA that is self-directed, or one with a checkbook.

1. Liquidity

As a result, it is difficult for many assets to be sold quickly. Real estate, private businesses, precious materials, etc. are examples. When cash is required for an internal or external expense (or a distribution), selling the asset too quickly can be problematic. This could lead to further problems such as accidental commingling of funds. Owners of self-directed IRAs should perform thorough due diligence before committing their investment strategy.

2. The legal framework for a company’s formation

To form a Checkbook IRA first, a Self-Directed IRA LLC must be created. Next, just as with any business entity, the LLC will open a bank account. The IRA money is then transferred to the LLC’s checking account.

The IRA owner may be able to become the only managing member and signatory of the LLC with the right legal structure. Incorrect legal structure, registration or titling can all lead to serious issues for the tax advantaged status of an IRA. Many checkbook IRA facilitators are competent, but errors could always lead to issues and possible disqualification/loss of the entire IRA.

3. Reporting errors in transactions

A checkbook IRA allows owners to fund their investments rapidly and easily, however, they are responsible for following the rules, and reporting all transactions.

The owner of an LLC must provide the IRA custodian with complete details of all transactions at the end of every year. fair market valuation (FMV) information. A custodian will be more likely to report incorrect income on investments if they do not have oversight of each transaction. To avoid breaking the law, always ensure that the custodian is provided with accurate information.

4. “Deemed distribution” Treatment

This is a warning to clients who are considering buying digital assets or real estate. “deemed distributions” treatment. McNulty, v. Commissioner: A case from the United States tax courts. illustrates the considerable risks of maintaining a checkbook IRA. The McNulty Case involved a taxpayer who used her checkbook IRA LLC in order to buy gold from a dealer of precious metals. She kept the gold from her LLC at home, in a safe. She was found guilty of herfelony. “unfettered control” Her IRA was deemed to be taxable because she had not consulted a third-party about the gold in her LLC.

You can never know what a court of taxation will do. “deemed distribution” Any transaction or investment in a checkbook IRA will be treated differently. The McNulty decision could make your checkbook IRA taxed if you hold bitcoin keys in an unsupervised setup. Alternative investments are relatively new (2015) and have been included in the tax code. IRS Publication 590It’s possible the IRS or Congress will be more scrutinizing of checkbook IRAs in future. Read more about the McNulty case and its implications.

5. Transactions that are prohibited

It is against the law for any self-directed IRA owner to mix personal assets with IRA funds or use personal money to enhance IRA investments. “Self-dealing” This is a common mistake for those who have self-directed funds. For example, if you use your IRA to purchase real estate, you are not allowed to use the property yourself—not even a little bit. It is not allowed to rent out office space, live or stay in the property. Even if you want to build your own home, it is not allowed. own Repair or Provide “sweat equity.”

Not only the IRA owners are excluded from participating in IRAs. “self-dealing,” But spouses, kids, and grandkids are also eligible. These individuals are disqualified. penalties are stiff. If you violate these rules, it can lead to a lot of tax problems. This is not to crush your dreams, but putting your 401k/IRA money into an Airbnb home on a lakefront and having your family or you stay at the property even just once would be a terrible idea. It’s also not a good idea to buy an investment property and rent it out. See the IRS list of prohibited transactions here.

Here are several examples on how digital asset investors could benefit from the prohibited transactions rule:

- IRAs and Personal Wallets – Do not mix them up

- Without a Non-Recourse Loan, you can leverage your money

- You can invest in collectible NFTs1

6. Financing

It is more difficult to finance a self directed IRA for a number of reasons.

- For any real estate purchase, you will need a larger deposit and a loan without recourse.

- Unexpected fees and costs can quickly mount up, reducing profits.

- IRA-owned businesses that are active could be impacted by the issue of UBIT Unrelated Business Income Tax The overlap with bitcoin is affected. mining within an IRA.

- All income and expenditures must be contained within the IRA. Personal funds cannot be mixed in. When the water heater breaks down (real estate), or when salaries are due (businesses), then the IRA must cover the costs. own cash. IRA holders may be tempted temporarily to mix funds as they seek short-term liquidity in order to meet their needs.

What is the impact of bitcoin IRAs on investors?

Self-directed IRAs can pose many possible risks if they are not well managed. IRS and Congress pay special attention to abuses and misuses of these structures. Combine their desire to regulate digital assets with this, and it seems that the landscape is ready for more scrutiny. In order to avoid these pitfalls, bitcoin IRAs require a specific approach.

Unchained IRA Is Not A Checkbook IRA

Unchained IRA is a good option if you want to store bitcoins in your IRA. This is not an IRA. “checkbook IRA” Unchained’s key is used in the collaboration custody setup in order to track the inflows, outflows and IRA vaults. The visibility feature allows the custodians of the IRA to be able to track the IRA’s inflows and outflows and ensure users are compliant with IRA rules.

No self-reporting is required and the structure that does not use a checkbook helps reduce the risks of possible pitfalls. It is important to hold coins correctly in IRA structures if Bitcoin appreciates as investors anticipate.

You can also find out more about this by clicking here. article The information provided is for educational purposes, not tax advice. Unchained cannot provide tax advice. Please consult an accountant or attorney of your choosing for any questions regarding taxes. Jessy Gilger worked for Unchained at the time of this article, but now he works with Unchained affiliate Sound Advisory.

Collectibles, while technically not part of the Prohibited Transaction Rules of Internal Revenue Code (section 4975), are prohibited by section 408(m) from being kept in an IRA.

Original published by Unchained.com.

Unchained, the US Collaborative Custody partners of Bitcoin Magazine is also a sponsor for related content. Visit Unchained to learn more about the services they offer, their custody products and how Unchained is related with Bitcoin Magazine. our website.

“This article is not financial advice.”

“Always do your own research before making any type of investment.”

“ItsDailyCrypto is not responsible for any activities you perform outside ItsDailyCrypto.”

Source: bitcoinmagazine.com