Ethereum’s price has performed better than Bitcoin, particularly when looking at the time frame since Bitcoin was created, as well as halving and bull market years. ETH however has underperformed consistently since the bear markets in 2018-2019, and 2022-2023. Ethereum will be significantly behind Bitcoin in 2024, the year of the halving. It has actually been performing poorly against Bitcoin over the last three years.

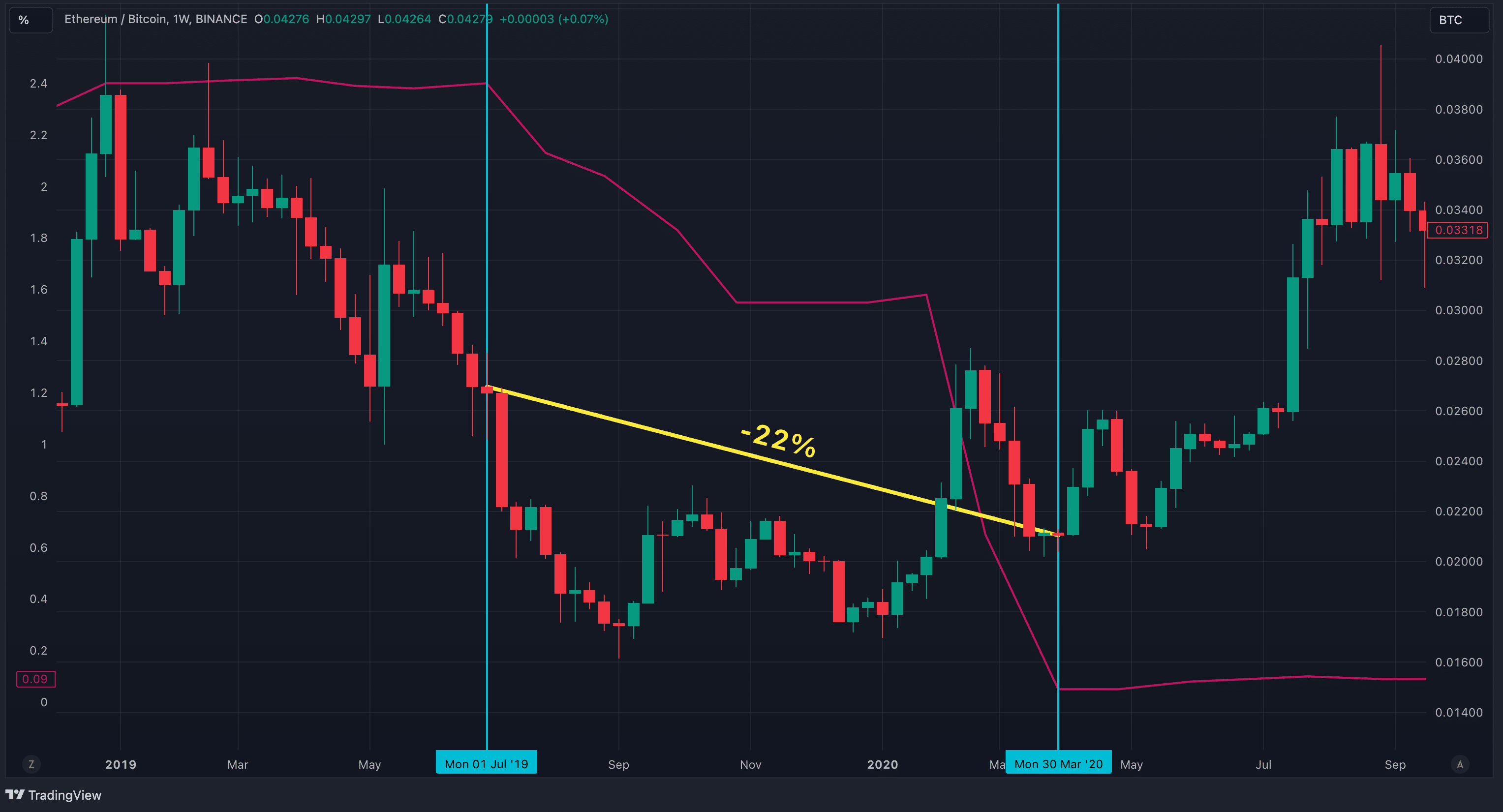

The ETH/BTC rate has plummeted to a 3.5-year high

While fractals aren’t a foolproof way to predict the future, their concept of similar patterns repeated over timeframes is a valuable tool for understanding what could be ahead.

In the previous halving year, the ETH/BTC rate broke through its support around December to September, and then began an upward trend in the first quarter the next bull market. The same scenario may unfold in 2024 as Ethereum is once again breaking through its support. The situation this time is far more alarming. The support level at 0.05 is much older than previous years of halving, when it was only a few years old. This suggests that Ethereum’s outlook has become more negative.

Another point of comparison can be drawn from 2019 when the Federal Reserve started cutting interest rates—a move that might recur in September 2024. From the Fed’s first rate cut until the Fed stopped it, in 2019 the ETH/BTC was down by 22 percent.

In all cases the ratio dropped, and Ethereum’s own price also fell, with 2020 being an exception. But the real question isn’t whether the price rose or fell, but if holding Ethereum was a good investment. History has shown that, in similar circumstances, holding Bitcoin proved to be the more advantageous choice—and 2024 may very well continue that trend.

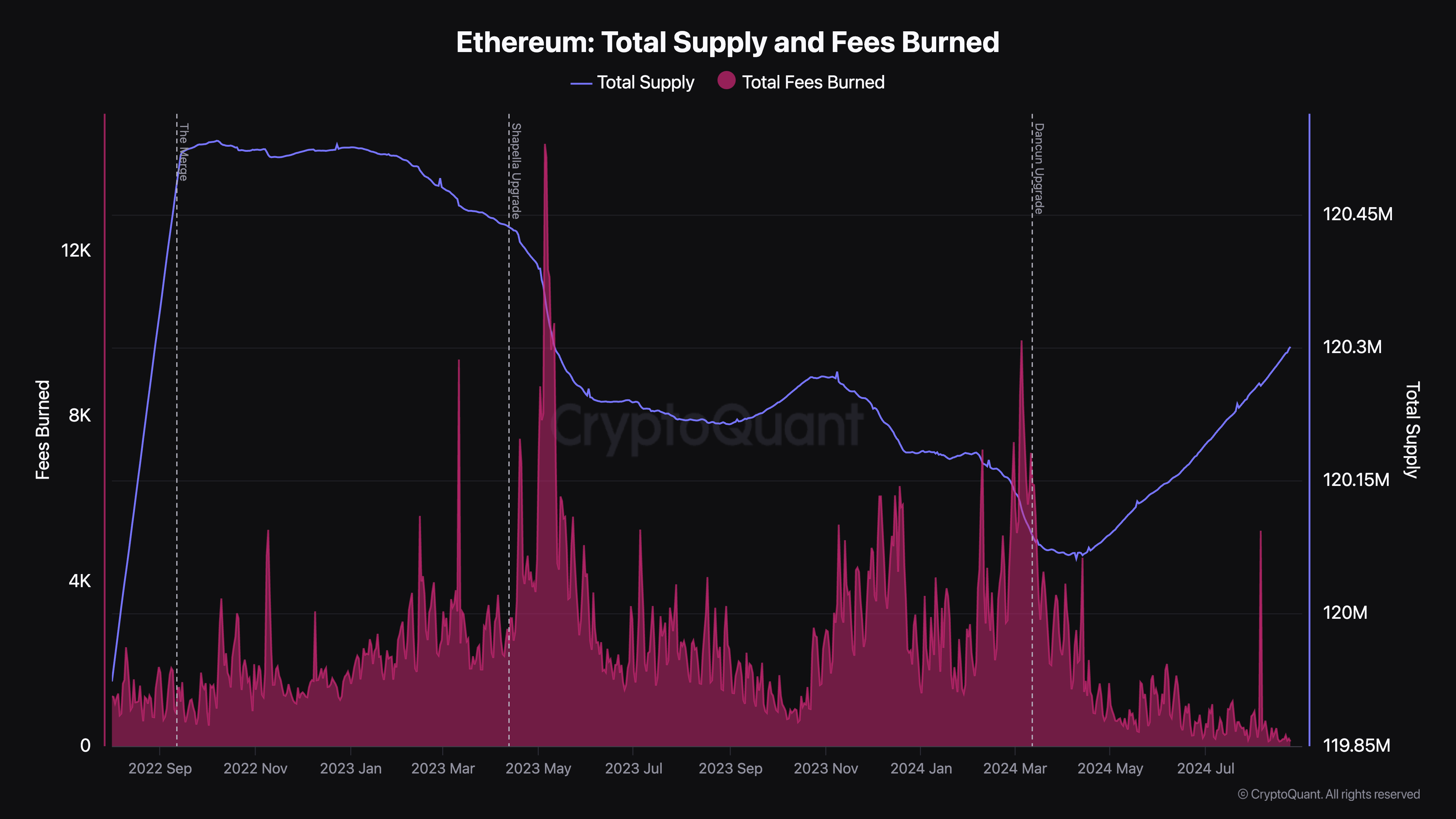

Ethereum’s supply reverses and becomes inflationary

Since the 2022 Merge, Ethereum supply has been steadily decreasing. This decrease is achieved through the mechanism known as “burning,” The Ethereum Improvement Proposal (1559) was released in August of 2021. Basically, a part of the transaction fee paid in ETH will be permanently removed or burned. It reduces ETH supply over time.

After the 2022 Merge, the Ethereum supply started to decline because the network switched from an proof-of-work A proof-of-stake consensus mechanism. Under PoW new ETH would be continuously distributed to miners in exchange for validating the transactions. This increased Ethereum’s supply. With the Merge, and subsequent switch to PoS the issuances of new ETH have decreased significantly. This is because the validators who secure the network now receive lower rewards than miners.

Dencun upgrade The turning point in March 2024 reversed this trend of deflation and made Ethereum supply inflationary. It introduced protodanksharding. “blobs,” This optimizes the data storage, and also reduces transaction costs on layer-2 networks. Dencun increased scalability while making transactions cost-effective. It also resulted in a large decrease in the amount ETH that was burned.

Since the Dencun, Ethereum has seen its supply increase. Over 213.5K new ETH have been added into circulation. upgrade. Ethereum supply has now reached the level of May 2023.

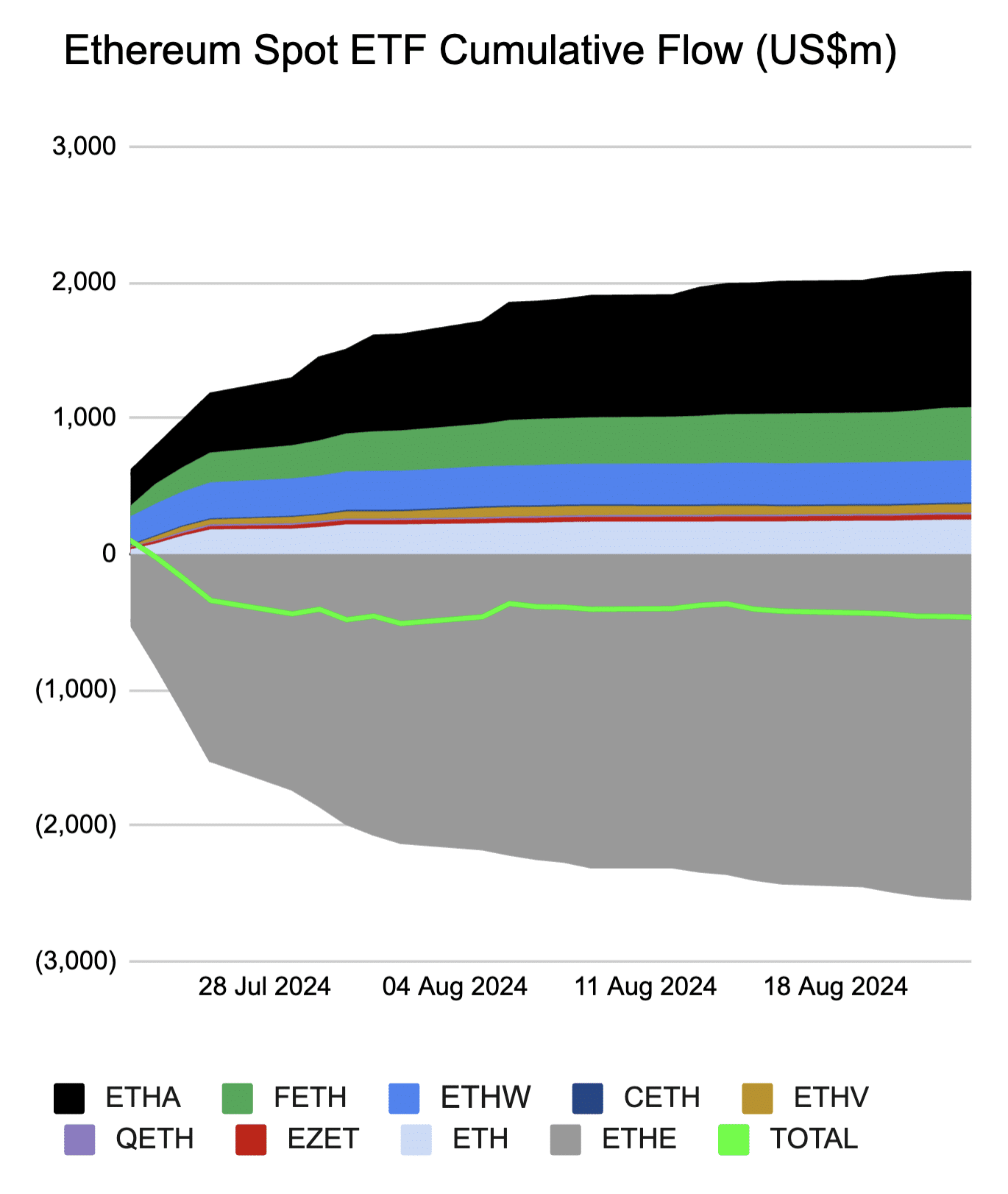

ETFs continue to flow in a negative direction

Many believed that Ethereum ETFs approval would increase ETH’s value by driving up the price. But this is not the case. ETF outflows are a bigger concern. A total of $465 millions has been withdrawn since the trading started. Grayscale ETHE is the main culprit, as it has experienced massive outflows that have overshadowed the positive inflows of other Ethereum ETFs. ETHE has seen such large outflows that they have created a net-negative effect for all Ethereum ETFs.

The Ethereum ETF is a fund that holds Ethereum in a specific amount. Each of the shares represents a portion of this total. Demand from investors can drive the ETF price above the value of Ethereum. The Authorized Participants (APs) are large in this scenario. financial Institutions work Step into the picture, working closely with ETF providers. They buy ETH from the open market, exchange it for ETF shares with the ETF providers, and then resell them to market investors at a higher rate, earning a profit. This process helps to increase the number of ETFs, which in turn brings the price of shares back into line with that of the assets.

In the opposite case, when the ETF is in low demand, its price may fall below that of Ethereum. Here, APs can buy undervalued ETFs from the marketplace, then return them back to the ETF provider and get Ethereum as a result. Arbitrage profits can be made by selling Ethereum to the public at a higher rate. It reduces ETF share supply and aligns price more closely with Ethereum’s value.

Simply stated, the ETH sold by APs when they redeem ETFs shares may be the reason why ETH’s price has been down.

The conclusion of the article is:

Ethereum remains fundamentally strong, even if current data suggests otherwise. Number of addresses active on its Layer 2 and main chain networks continue to grow. Ethereum is still the leader in the blockchain sector, and holds the number one spot for total value locked (TVL), across all DeFi platforms. Many projects are being developed using its ecosystem. Ethereum is also undergoing regular upgrades and development.

Ethereum, however, may not make the most sense in the short-term, particularly for the remainder of 2024, due to the market conditions. In 2025 however, Ethereum could regain its previous momentum, and outperform Bitcoin once more in terms of return, just as it did in past market cycles.

Disclosure article This is not investment advice. This page is intended for informational purposes only.

“This article is not financial advice.”

“Always do your own research before making any type of investment.”

“ItsDailyCrypto is not responsible for any activities you perform outside ItsDailyCrypto.”

Source: crypto.news